Between erstbezug, Comparis, and a few housing trade shows, at the beginning of the year I was swimming in neubau options. We had choices anywhere from 2 room to 6.5 room flats with terraces or gardens, but location and cost made it difficult to weigh the options.

It seemed like almost anything within the city limits of Zürich was priced at one million plus, no matter how far away from public transportation it was. And most of the loftier 5.5-6.5 flats were in towns 45-60 minutes to Zürich by bus and train, which was further than we were willing to move.

Erstbezug helped me find a few building sites near Zürich with flats that actually fell in an affordable range. From the project pages I was able to go through each of the flats at a building site and look for something in our size and price range.

The race came down to two flats/building sites, where I mulled over the possibilities over and over.

Flat A:

I found the Flat A project almost at the beginning of my housing search at the end of 2011. The flats were still pretty expensive for the space you get, but the location had so many good things going for it and the flats looked amazing.

Image via Homegate.ch

The Good:

- 10 minute train ride to Zürich main station

- Train, tram and bus lines available

- Direct routes to the airport

- Large shopping center across the street

- Remarkable 90sq m (968 sq ft) balcony in some flats

- Finished in summer 2013

- My commute only increases by 5-10 minutes.

- Kay’s commute would but cut in half

The Bad:

- Still pretty damn expensive

- Not sure how much we actually save much by moving

- Only 3.5 rooms, meaning we will definitely outgrow it if we start a family.

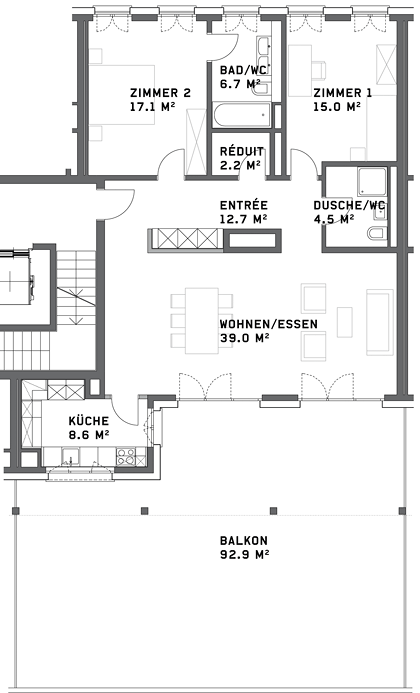

Flat B:

I found the Flat B project a couple months into my search. It was a relatively new project and most all of the flats were free. If we chose to go with a 3.5 room flat with 20sq m (215sq ft) less than flat A, we could stand to save 250,000CHF on the price of the home.

Or if we paid the same as Flat A, we could upgrade to a 5.5 room flat with 20sq m more than Flat A. Decisions, decisions.

Image via Homegate.ch

I couldn’t stop imagining a bedroom, walk in closet room, guest room and office…

The Good:

- So. much. space.

- Value for money

- Possibility to save a ton per month if we stuck with a 3.5 room

- Parking spaces were a few thousand cheaper than Flat A

- Kay’s commute would stay the same

The Bad:

- 15 minute walk to local train stop

- 25 minute total commute time to Zürich main station, not great.

- Only the far away train and an unhelpful bus route nearby

- Smaller terrace than Flat A

- No groceries nearby, no large groceries at the train stop

- Finished autumn 2013, getting a bit late

- My commute would increase from 30 minutes to 1 hour one way.

During the whole process of looking for flats and trying to convince Kay that buying was a good idea, we missed out on a cheaper option in the building of Flat A. There was another 3.5 room flat the same size, but with a smaller (but still sizable!) 25 sq m (269sq ft) balcony and a small loggia that was selling for about 100k less than Flat A. I would have chosen it to save money, but shortly after we visited the showroom, the flat was already reserved.

The problem with building A was that we were a bit late in discovering it. Half the apartments had been purchased already and I could tell that there were larger 4.5 and 5.5 room flats that had gone for less than the price of Flat A. Hell, there were other 3.5 room flats that had gone for 250,000 less!

I felt like we were slightly too late with Flat A and that if we really wanted to capitalize on being an early bird, we could do that with Building B where all the flats were ripe for picking at good prices. I was also beginning to worry that we would overstretch our budget with Flat A and that it would be better to choose a much cheaper 3.5 flat in building B. Our mortgage would be sooo much cheaper with 250k less in debt!

Can you tell which flat which chose?

Want to catch up?